Media

HKU Announces 2014 Q2 HK Macroeconomic Forecast

09 Apr 2014

Economic Outlook

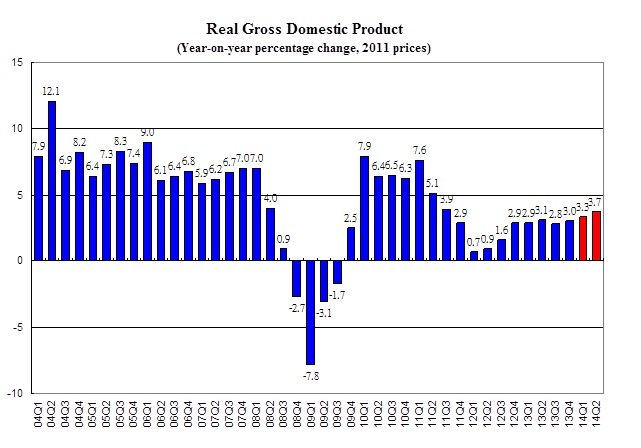

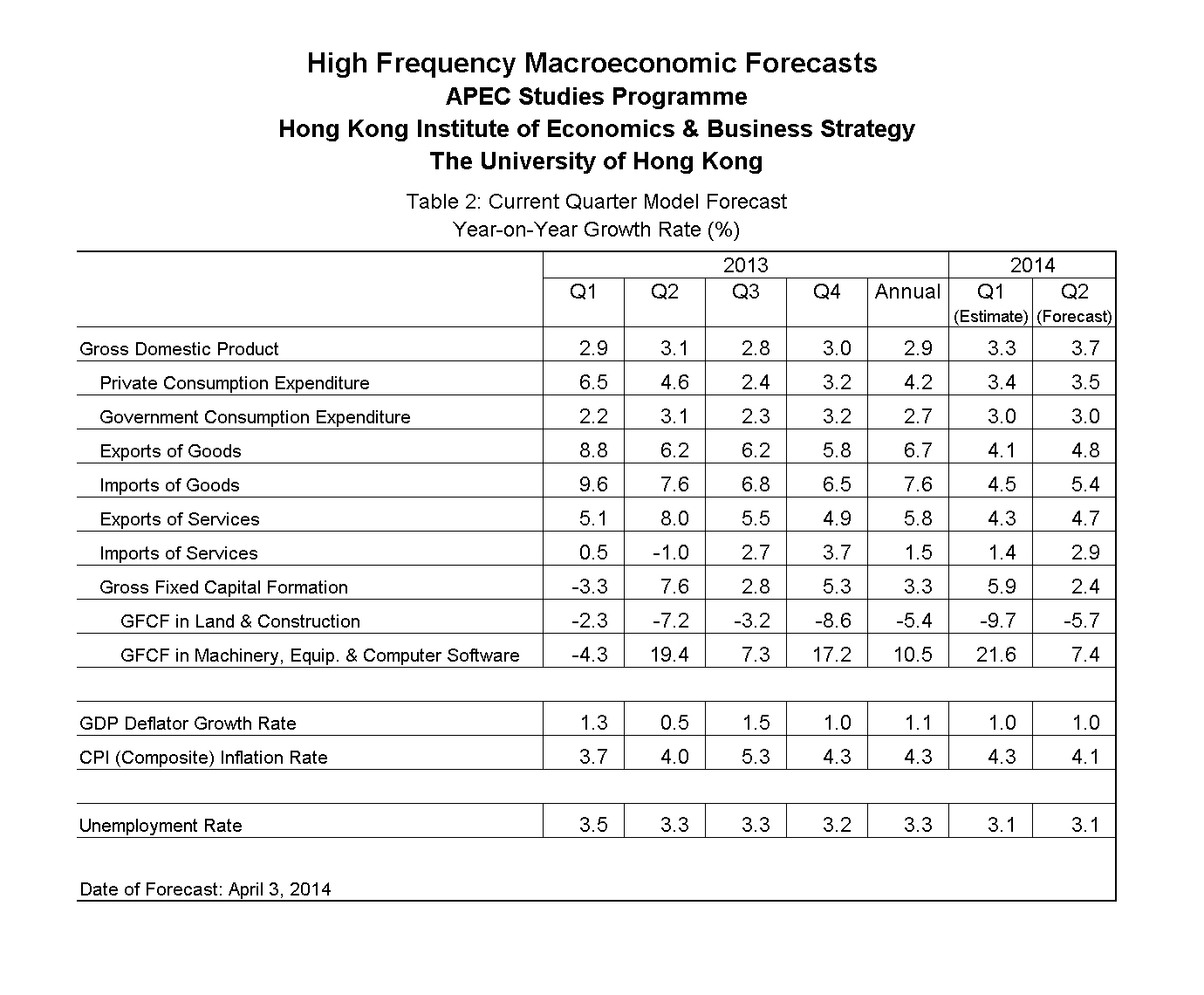

The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong Kong (HKU) released its quarterly Hong Kong Macroeconomic Forecast today (April 9). According to its High Frequency Macroeconomic Forecast, real GDP in 14Q1 is estimated to increase by 3.3% when compared with the same period last year. This is a slightly downward revision of our previous forecast of 3.5% growth released in January 9, 2014. This adjustment reflects a mild delay in the recovery of external demand due to the harsh winter in North America as well as the statistical revision by Hong Kong Census and Statistics Department. In 14Q2, real GDP growth is forecast to rise by 3.7% when compared with the same period last year.

Professor Richard Wong Yue-Chim, Professor of Economics at HKU said that, "Hong Kong underwent a mild recovery in 2013 after the hit of the European sovereign debt crisis. Real GDP grew by 2.9% last year. , The performance in 2013 was impressive when compared to the 1.5% growth in 2012 but was modest when compared to the average of the past decade. The on-going strong growth in the Mainland provides the underpinning of sustained growth in the local economy. Desirable job market, high consumer sentiment and continuity of infrastructural projects will continue to support Hong Kong economic growth in 2014. The pace of Hong Kong's real GDP growth is forecast to accelerate and grow by 3.5% in the first half of 2014, up from the 2.9% growth in the second half in 2013. Domestic demand remains the main driver of economic growth."

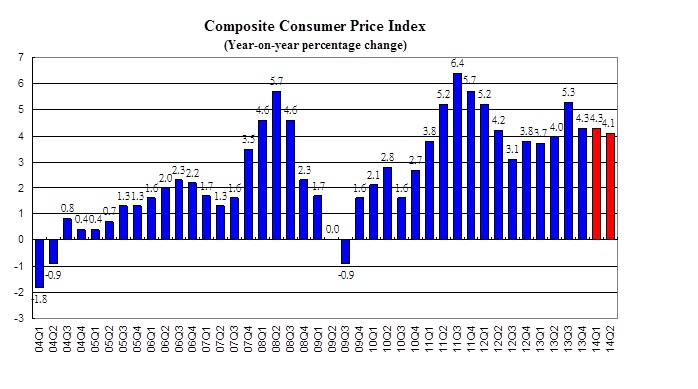

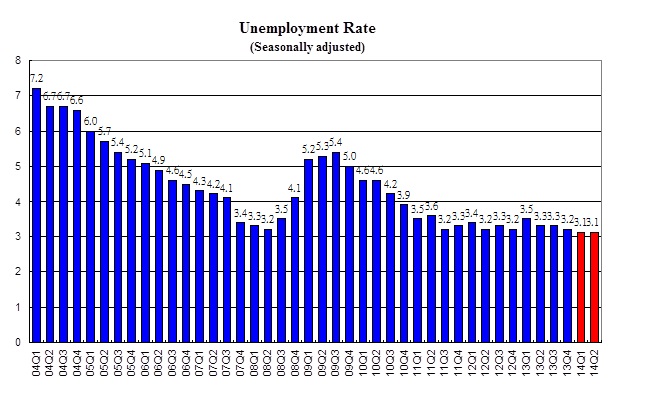

"The job market is expected to be vibrant, with the unemployment rate forecast to stand at 3.1% in 14Q2, same as 14Q1. Inflation is expected to ease in the near term, brought by stable food prices and rental rates. The headline consumer inflation rate is forecast to be 4.1% in the second quarter, down from the estimated 4.3% in the first quarter," according to Dr. Ka-fu Wong, Principal Lecturer of Economics at HKU.

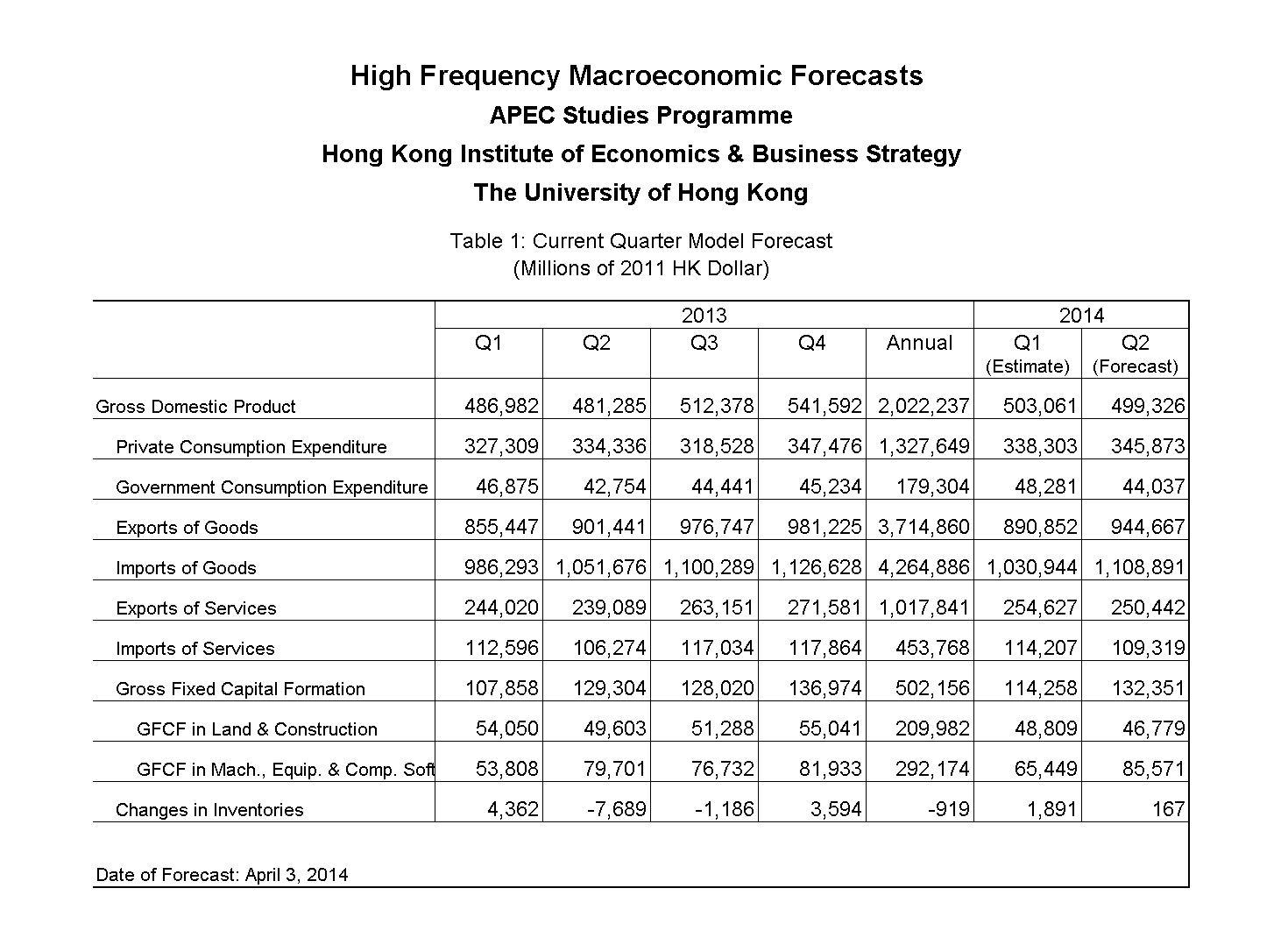

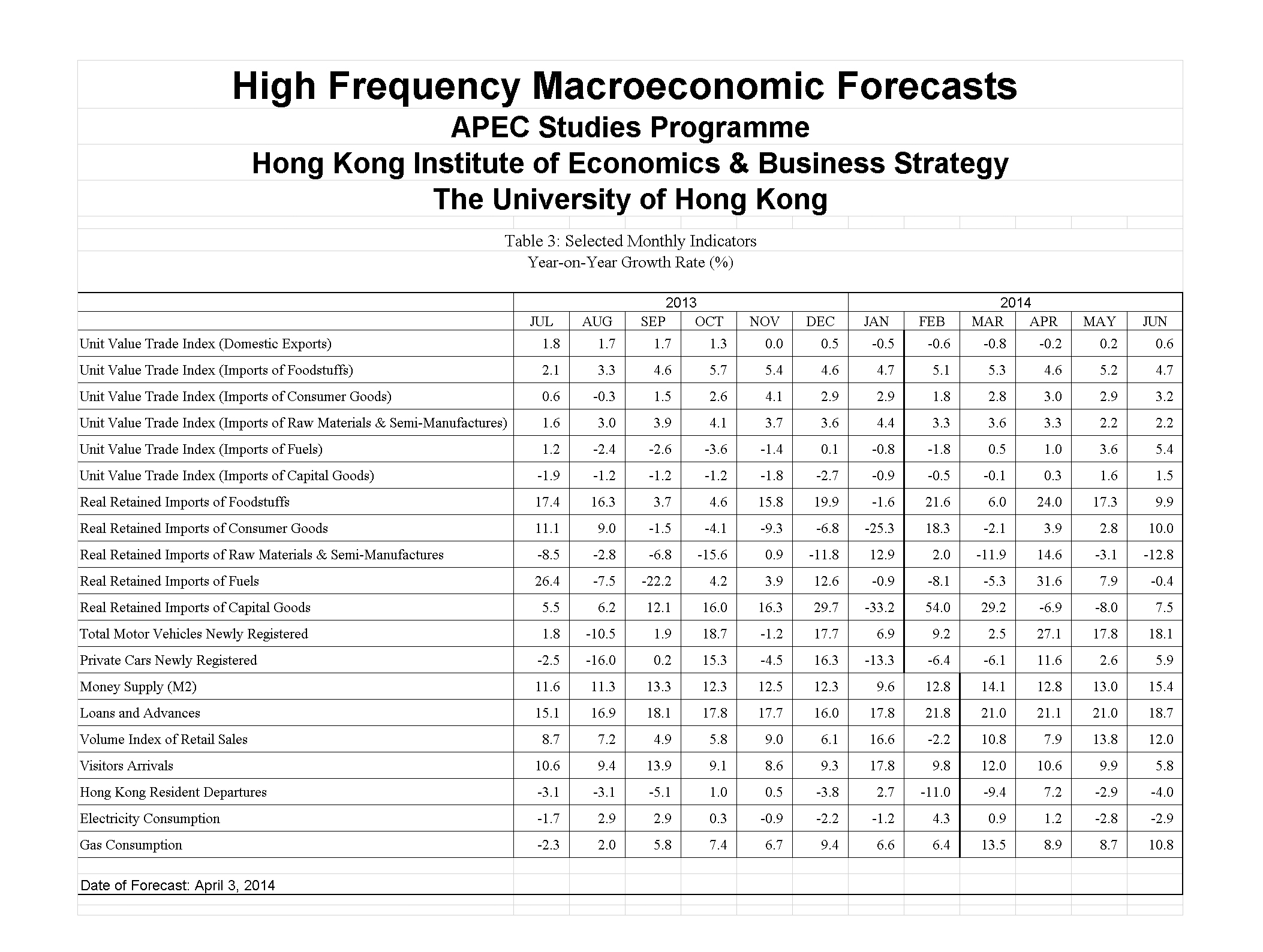

The forecast details are in Table 1 and Table 2, and the forecasts of selected monthly indicators are in Table 3. All growth rates reported are on a year-on-year basis.

Forecast Highlights

{kind=link}

{kind=link}

{kind=link}

- Given strong economic growth, stable job market and buoyant consumer sentiment, private consumption spending is projected to continue to grow. The growth of real average payroll, increased by 1.0% in 13Q4, continues to fuel consumption. Consequently, private consumption is forecast to grow at 3.4% in 14Q1 and 3.5% in 14Q2.

- The volume of retail sales grew by 7.9% in the first 2 months of 2014, and is projected to continue to grow in the next couple of months, supported by local wealth effect of payroll increase, as well as the continued strong growth in visitor arrivals. The volume of retail sales is forecast to grow by 8.8% in 14Q1 and by 11.2% in 14Q2.

- Total exports of goods in real terms grew by 5.8% in 13Q4, decelerating from the 6.2% increase in 13Q3. Boosted by US and European recovery, the growth momentum is projected to continue. The total exports of goods in real terms is estimated to grow by 4.1% in 14Q1 and 4.8% in 14Q2.

- Imports of goods increased by 6.5% in 13Q4, decelerating from the 6.8% growth in 13Q3. The imports of goods is forecast to increase by 4.5% and 5.4% in 14Q1 and 14Q2 respectively.

- Service exports grew by 4.9% in 13Q4, slower than the 5.5% growth in 13Q3. The pickup in visible trade boosted the demand for trade-related services. The strong growth in visitor arrivals also provided further support for the growth of service exports. Indeed, the visitors from the Mainland rose robustly by 14.1% in the first two months of 2014. For every 5 visitors, there were around 4 persons coming from Mainland currently. The increase in service exports is forecast to grow by 4.3% in 14Q1 and 4.7% in 14Q2.

- Service imports increased by 3.7% in 13Q4, picking up from the 2.7% increase in 13Q3. Outbound tourism incentive was dampened by uncertain political situations in various countries. Therefore, the growth in service imports is expected to be slower. It is forecast to grow by 1.4% and 2.9% in 14Q1 and 14Q2 respectively.

- Gross fixed capital formation rose by 5.3% in 13Q4, picking up from the 2.8% growth in 13Q3. Projected economic growth and infrastructural projects will continue to support investment spending. Gross fixed capital formation is forecast to grow by 5.9% in 14Q1 and 2.4% in 14Q2. A year earlier, in 13Q2, gross fixed capital formation grew by 7.6%. Thus, the slowdown in 14Q2 is partly due to a higher base of comparison.

- Investment in land and construction dropped by 8.6% in 13Q4, worse than the 3.2 drop in 13Q3. This category is expected to remain subdue due to the lack of new infrastructural projects and cautious private investment, with the decline projected to be 9.7% in 14Q1 and 5.7% in 14Q2.

- Investment spending in machinery, equipment and computer software grew by 17.2% in the 13Q4. Underpinned by the continued economic growth and optimistic business confidence, investment in machinery, equipment and computer software is projected to increase by 21.6% in 14Q1 and 7.4% in 14Q2 when compared with the same period last year. The surge in 14Q1 was partly caused by comparing to a lower base in 13Q1, in which a 4.3% decline was recorded.

- The general price level, as measured by the composite CPI, rose by 3.9% in February 2014, with food and housing contributed 1.2 and 1.8 percentage points respectively to the overall increase. These two items accounted for 77% of the total increase in the general price level in February 2014. Inflation is expected to be stable in the first half of 2014. The headline consumer inflation rate is forecast to be 4.3% in 14Q1 and decrease to 4.1% in 14Q2.

- The provisional seasonally adjusted unemployment rate stood at 3.1% in the three months ending in February 2014. The job market is expected to continue to be stable. Rising real income encourage individuals joining the labour force, reaching almost 4 million persons in current quarter. In 14Q2, the 16,000 increase in the number of employment is expected to offset the negative impact of the 9,000 increase in the number of unemployment. The unemployment rate is forecast to stay low at 3.1% in both 14Q1 and 14Q2.

Concluding Remarks

Our major trading partners continue to exhibit stable growth or be on track of recovery. Despite the bumpy recovery partly due to the severe weather in the beginning of 2014, US output growth is gathering steam and is expected to expand in latter part of 2014. With the gradual improvement of 6.7% US unemployment rate, US monetary policy can tighten, but unlikely drastically. In China, output growth target of 7.5% in 2014 seems achievable. In addition, stabilization in the Euro-zone has been basically confirmed.

Putting all these factors together, Hong Kong is expected to continue its growth at a faster pace of 3.5% in 2014 annually, comparing to the 2.9% growth in 2013. Meanwhile, we will closely monitor the recent USD appreciation against RMB and political uncertainty developing in the Asian Pacific area.

About Hong Kong Macroeconomic Forecast Project

The Hong Kong Macroeconomic Forecast is based on research conducted by the APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at HKU in the Faculty of Business and Economics. It aims to provide the community with timely information useful for tracking the short-term fluctuations of the economy. The current quarter marco forecasts have been released on a quarterly basis since 1999.

The high frequency forecasting system was originally developed in collaboration with Professor Lawrence Klein of the University of Pennsylvania in 1999-2000. Since then, the system has been maintained and further refined by the APEC Study Center which is now a research programme area of the Hong Kong Institution of Economics and Business Strategy.

The project is sponsored by the Faculty of Business and Economics. The Hong Kong Centre for Economic Research at HKU provides administrative support to the project. Researchers at the Hong Kong Institution of Economics and Business Strategy are solely responsible for the accuracy and interpretation of the forecasts. Our quarterly forecasts can be accessed at: http://www.hiebs.hku.hk/apec/macroforecast.htm

For media enquiries, please contact Ms Trinni Choy, Assistant Director (Media)

(Tel: 2859 2606/Email: pychoy@hku.hk), or Ms Melanie Wan, Senior Manager (Media) (Tel: 2859 2600/Email: melwkwan@hku.hk), Communications & Public Affairs Office, HKU.